Saturday, January 12th, 2019 | The Cash Flow Group | Comments Off on How To Ask Questions.?!

Here’s the premise:

Good questions directly lead to greater success in life and career;

Most people ask bad questions (myself included).

We are constantly solving problems on the job, including making the sale. We need to collect information to solve these problems. How we ask questions greatly influences the answers and our eventual success. Better questions lead to better solutions, faster, leaving more time to accomplish other goals, solve other problems, or recreate.

Time is precious and opportunities are fleeting. Walking down the hall or riding in an elevator with your boss, their boss, or your client is the perfect opportunity to learn and/or impress with a great question. A poorly worded question means a missed opportunity.

In our personal lives, well structured questions lead to better conversations and deeper emotional connection. Fortunately, learning how to better structure questions is not that difficult.

Examples Of Bad Question Techniques

Ramble;

Ask leading questions;

Ask multiple-choice questions;

Pose Yes or No questions when you need information.

When your question goes on and on, the real question gets lost and so will the answer. Rambling is often the sign of nervousness, embarrassment that you don’t know the answer, or lack of forethought about your real question and how to ask it. If you need the answer, don’t be embarrassed to ask the question.

Bad: What’s the best way for me to calculate DSO? Do you want me to use all sales? Over what period? And should I eliminate cash sales? Do I look at the last month or longer? And what about receivables that we haven’t written off by they are really old? And that large contract receivable that the sales person said we should never have booked because of the dispute that emerged only days later?

Good: How do you want me to calculate DSO?

If you ask a leading question, you are not likely to get an honest answer, and therefore you are off-track in getting to your solution. Even if you think you already know the answer or are just seeking confirmation, an objective question makes you look more confident. A leading question can make you look like a condescending jerk.

Bad: What do you think about the ugly sample logos they presented?

Good: What do you think about the sample logos?

Multiple choice questions are appropriate when you truly want the listener to choose from one of the options. But, if you are trying to learn, have a conversation, or interview someone, you lose valuable time with your extended question and tend to limit the responses.

Bad: When you saw the presentation, what captured your attention the most? The graphics and video? The speaker’s great delivery and humor? The emotional customer testimonials?

Good: When you saw the presentation, what captured your attention?

When you want to learn, you don’t want to ask a closed ended question that can be answered with a simple “yes” or “no.” Instead, you want to ask an open ended question so the person can share their thoughts and you get information.

Bad: Did you like the movie?

Good: What did you think of that movie?

Top 2 Question Tips

Stop talking at the question mark;

H5W: How, who, what, when, where, why. Start with one of these words.

Stopping your question when you get to the question mark is the opposite of rambling or asking a multiple choice question. Too often we are trying to show our knowledge or cover up our lack of knowledge with extended questions. By simply focusing on this one technique of stopping at the question mark, you will start asking better questions.

Bad: Do you have any vacation plans this summer? I know you often go to the mountains, and you have been talking a long time about going to Europe. But, you said you haven’t seen your parents in a long time, so are you going to visit them? And, didn’t you say something about one of your kids maybe having to go to summer school, so will that interfere with plans?

Good: What are your summer vacation plans?

How, who, what, when,where and why has been the staple of reporting since the infancy of journalism. It also turns out to be a better way to ask questions. Start your question with one of these 6 words, and you are more likely to get thoughtful or more revealing answers. Alternatively, journalist Shane Snow says sentences “that begin with is, are, would, should or do you think can limit your answers”. All too often these words result in leading or closed ended questions and an answer of less value.

Bad: Should the government add more laws restricting gun sales?

Good: What do you think of the current laws on gun sales?

When I’m preparing for a meeting or conversation where I know I’ll be asking a lot of questions, I’ll write on a sticky note or in my notebook:

? Stop H5W

I look at this frequently to remind myself to keep my questions in check and start with the right word.

How To Use Questions

Get Conversations Back On Track

Questions can be used for more than just learning and solving problems. Think about the interviews you’ve heard. The guest may start rambling or drift off-topic. You start to lose interest. A skilled interviewer can interject with a good question to get a conversation back on topic without seeming pushy or condescending. You can use this same technique in meetings, phone calls or personal conversations.

Sell Ideas

We all know that a great way to get buy-in to something is for the person to think it is their idea. A series of questions can get someone to see things from your perspective or arrive at the solution you desire. You don’t need to ask leading questions, just well designed objective questions. You will get better ideas and less resistance. Follow up with comments and more objective questions until their answers point to your desired result. Suddenly, it’s their idea. While this approach seems to take longer and require more effort, questions help you avoid defensiveness and resistance and often this is the fastest way to your desired result.

Resolving Disputes

I’ve been negotiating transactions and resolving disputes for over 30 years. Asking questions is one of my favorite and most successful techniques. I know that initially I have limited knowledge of the situation, and that is usually heavily weighted towards my client’s perspective. But, I can’t get a deal done or a dispute resolved until I can get both sides to the same place. Questions help me learn and people like to be heard, which is a critical step in resolving problems. If the initial answers and facts support my client’s position, I find asking additional questions is a very effective way to get the other party to an acceptable resolution.

At our collection agency, I frequently deal with clients whose customers don’t want to pay for the full amount of a long term contract. The most common reasons are: they don’t need the services any longer, they weren’t getting the sales results desired from advertising or marketing services, they didn’t cancel before it auto-renewed, or they’ve run into financial problems. The most common excuse is that our client failed to perform. Once I learn their position and underlying rationale, I’ll ask questions:

Where in the contract does it say you can cancel?

Where in the contract does our client guaranty market results?

When did you first realize there might be a performance issue?

Where is your written documentation and notice of performance failure?

What does the auto-renewal language say?

Where is your written cancellation notice?

I find that by asking questions instead of making assertions, there is less resistance, more focus on the specific point, and a realization that their legal position is precarious. They may not admit any weakness, but as long as they understand, progress has been made and the specific issue no longer needs to be addressed. Now we can focus on negotiations and a resolution.

Questions As A Negotiating Tactic

You can’t resolve a dispute if you are stuck on positions.

A few years ago a small businessman called me after his $300,000 project with a public company blew up at the last moment. Days before the project was to be completed, the legal department at the public company noticed some paperwork issues they wanted to rectify. They passed along their requests to their project manager who communicated with the vendor. While the requests seemed very reasonable to the legal department, there were a variety of reasons why they were not reasonable to the vendor. The vendor said “no” to the project manager, the legal department said “no deal” to the project manager, and a minor disaster resulted.

I got involved when the customer was demanding the return of their deposit and the vendor wanted full payment of the remaining contract balance since he had essentially fully performed. After weeks of collecting information and phone calls with the customer, I finally pieced together what happened. Regardless of the specific issues between the companies, a stalemate had ensued and the project failed because during the dispute, each side had developed a position and simply kept repeating it.

The breakthrough in my attempt to resolve the dispute came when I asked the following question to the general counsel of the public company: ‘Why didn’t someone from your department talk directly with the vendor to understand his concerns and explore alternatives?’ The attorney realized the mistake and became more open to take a different approach in the current discussions. It took some tough negotiating from there, but we eventually found a way to avoid the courtroom and my client was satisfied with the final monetary compensation.

Questions Turn Focus From Position To Underlying Objective

As in the stalemate example above, I see this Position Problem in negotiations all the time. The parties focus on positions and not on what they want to accomplish. Whether it’s an acquisition, investment, intellectual property license, or debt collection, when you get stuck on positions, you are not likely to complete a deal. All too often, each side assumes it is a zero-sum game and that moving from their current position is a loss for them and a win for the other side. That usually isn’t the case, as getting a deal done is how each side actually gets a win, and the worst thing that can happen is each side remains stuck.

Knowledge is Power

This cliche is especially true in negotiations and dispute resolution. Both sides know it and may intentionally attempt to limit the knowledge you gain or mislead to get an advantage. You typically only get a limited amount of time and number of questions to ask. The amount of knowledge you gain will be directly tied to how well you ask questions.

Preparation is an extremely valuable part of the process. I try to learn as much as I can before a negotiation session or debt collection call. This way I can focus my questions on the areas where I have limited insight or knowledge and fill in the gaps so I can devise a strategy to achieve success.

Early in my career, I would ask leading or multiple choice questions because I thought I already had certain knowledge from my research and preparation. I wanted to race to the finish line from that starting point. All too often, despite my poorly worded questions, I would learn that my assumptions were wrong and there were other reasons that lead to the dispute. Or, worse, people would go down the path of my leading question and it would be much later before I learned of the other underlying issues and concerns. So, while preparation is key, I now focus on asking questions in a better way so I get more valuable answers.

Saturday, January 12th, 2019 | The Cash Flow Group | Comments Off on “That Employee Did Not Have The Authority To Sign That Contract” and how to handle hearing it.

“That Employee Did Not Have The Authority To Sign That Contract” At he Cash flow Group we hear it all the time: “We are not going to pay those invoices because the person who signed the contract didn’t have authority.” Many go on to say: “It says right in our By-laws that only an officer can bind the company.”

This tells us several things:

The debtor does not want to pay;

The debtor is aware of this outstanding payable;

There is a good chance the debtor has the money to pay;

The debtor either does not know the law or is pretending to not know the law.

As a south Florid collection agency specializing in large claims, we know the law is on our side. But, our initial response to “That Employee Did Not Have The Authority To Sign That Contract” is not about the law, but to ask questions to learn more. We want to know why they don’t want to pay, because that is the real problem to solve.

We encounter this situation most frequently with service contracts. Typically the debtor signed up for a service of some type, such as advertising, email list access, or an information database. The most frequently explanations we hear as to why they don’t want to pay are:

We never used the service;

We didn’t get any benefit from the service;

The service didn’t work the way we thought it would;

Our business changed directions and we didn’t need the service;

Our revenue declined and we just can’t afford it.

Once we hear the explanation of why “That Employee Did Not Have The Authority To Sign That Contract”, we’ll ask a few more probing questions to fully understand the real issue we need to resolve. We also make sure to contact the client regarding the debtor’s actual usage of the service in case that information will help us with the debt collection effort.

Then we pivot to the issue of Apparent Authority, the excuse the debtor is trying to hide behind. Under the law of agency, an Agent (employee) is able to bind the Principal (company) in a contractual relationship with a third party (customer or vendor). Business could not function efficiently if purchasing people could not order supplies and if sales people could not quote prices and complete sales. While these employees may not be Agents of the company able to execute a contract to sell the entire company to someone, they typically do have the authority to bind the company to these daily transactions.

Under Apparent Authority, if it appears that the employee has authority then their actions bind the company. This appearance can be accomplished by providing the employee with company identifiable forms or stationery, a truck with a company logo, or just having them work from the company office. In all of these cases, it is reasonable for the other person to assume that this employee has authority to enter into the transaction being discussed and therefore the threshold of Apparent Authority has been met. Our client’s contract with the debtor is legally binding.

Our collection strategy will be different if we are dealing with a sophisticated business person who is just trying to show us with a bad excuse versus an unsophisticated business person who is just hoping this excuse will work. So, we typically don’t just explain the concept of Apparent Authority, but ask a series of questions to learn more about who we are dealing with while leading the debtor to this conclusion.

For example of “That Employee Did Not Have The Authority To Sign That Contract”: how many people work for the company, who purchases the office supplies, who makes the sales, where do they work from, do they have business cards or access to company stationery, do they bind the company to these transactions? From there it is easy to explain Apparent Authority and volunteer to send them links on the Internet where they can see for themselves that this is a binding contract. From that point forward, we refuse to discuss that issue and get back to the real issue of collecting the money that is legally owed.

Saturday, January 5th, 2019 | The Cash Flow Group | Comments Off on calling your customer about a past due invoice

You have been calling your customer about a past due invoice for the last month. After a couple excuses and a couple broken promises, now no one answers the phone or returns messages when you call repeatedly. What does this mean? Have they closed? Has office staff been reduced to the point there is no one to answer calls, including from potential customers?

In our experience, it is not uncommon for us to learn that they are simply not answering calls from people who might be trying to collect money. So, any ID blocked calls, and calls from known creditors are always ignored, sent to voicemail, and never returned. This is especially true when calling your customer about a past due invoice on that person’s cell phone. We know this because we frequently get through to these people by using a phone number that the debtor will not recognize and they answer.

When implementing this strategy, we usually first call with our regular unblocked phone number and get the typical ignoring treatment. Then 10 minutes later we call with an unblocked but unidentified number. That way we know that the only reason they answered is they didn’t know it was not us who was calling.

As a collection agency, if someone answers an alternative phone, we know that this may be the last time we get to talk to the person. We very quickly deliver a firm message that we have now proven they have been ignoring us, and that if they do that anymore, we have no choice but to send their file to the attorney. For an in house debt collector, the message should be that their file will be sent to a collection agency and reported to credit bureaus and groups if that has not yet happened. We find that people are more likely to answer if the unidentified phone has an area code from the same region as the debtor. But, we find even cross country area codes can work, now that people keep cell phone numbers as they move about the country.

There are many ways to get low cost access to an unidentified phone for calling your customer about a past due invoice number. For under $20 initial cost, and as little as $10 a month, you can have a prepaid cell phone with any area code in the country. That’s a small investment to be able to get through to one or more customers who owe you money and are ignoring all your calls.

Once you get through, if you don’t get cooperation, you know you will never get paid unless you take other action. Just having that knowledge earlier is well worth the minor cost of getting an alternative number. We all know that the chances of collecting decline dramatically the longer an invoice is not paid.

So, the sooner you know they are ignoring you, and the sooner you take more aggressive action, the more likely you can still get a recovery.

Saturday, January 5th, 2019 | The Cash Flow Group | Comments Off on End of Year Tasks for your Business

The end of the year always brings some predictable events. You know that magazines and websites will be releasing their lists of “best movies” or “most memorable events.” You know that car dealers and other large item retailers will be trying to sell off expensive merchandise. You know payroll departments will be preparing to fill out W-2 forms, and accountants will be getting ready for tax season. As a commercial collection agency there are certain tasks we’d love to see business owners add to their annual end of the year to-do lists.

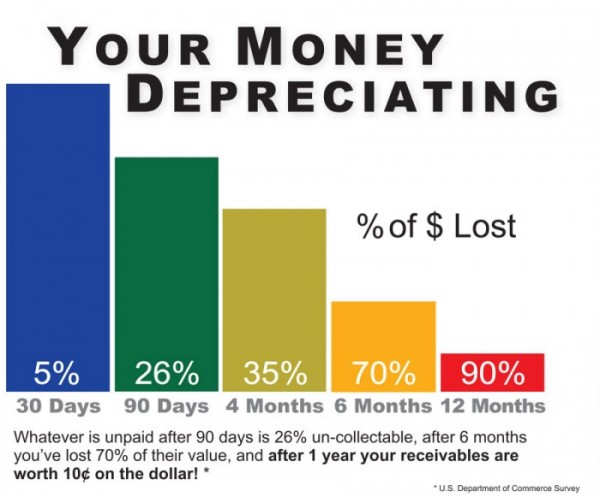

Determine Which Invoices Need Attention Once an account is 90 days overdue, there’s already a 26% chance that it will never get paid. At 7 months overdue, there’s only a 50% chance that you will get paid. Ideally, business owners would routinely check for late invoices and turn them over to a reputable collection agency while there was still a great chance of getting the invoice paid. But at the very least, reviewing past due invoices is something that should be end of year tasks for your business.

Update Terms and Conditions The world has changed a lot in the last five years. If you haven’t updated your terms and conditions on credit applications recently it may be time to make a change. Our free handbooks on Credit Applications and Terms and Conditions may not be the books you want to cozy up with by the fire, but they may save you money in the year ahead.

Review Procedures Are your internal collection policies and procedures working? Can you make changes to improve efficiency and effectiveness? Are you making phone calls when you should be writing emails to get answers in writing? Are you writing emails when you should be making phone calls? Is there anything you could automate, such as overdue notices, which would make life easier for your Accounts Receivable department? An annual review of your policies and procedures may help you identify both problem areas and strengths.

Update Payment Procedures Strangely enough, many businesses, especially smaller ones, often make it difficult for clients to pay them. If you’ve resisted allowing online credit card transactions, or PayPal transactions because of fees, it’s time to rethink those ideas. Services such as PayPal and Square may make your business more time efficient. Don’t forget to update your check payment procedures as well. Services like Vericheck can help you avoid accepting bad payments.

Check on Your Providers When you hire a lawyer or a credit collection agency you’re hiring a company that will represent you. The last thing you need is someone from outside your company creating legal or reputation hassles for you. Your end of year tasks for your business is a great time to check in with the reputation of any service provider that represents you. Check Better Business Bureau ratings, online reviews, and professional organization memberships.

The end of the year is a busy time and adding more “to dos” to your existing task list can be daunting. But, making sure that you’re on top of unpaid invoices and payment policies can be a great way to ensure that you start the next year off right. If you’re end of the year tasks reveal debts you need help collecting, make sure to let us know, we’re here to help.

Thursday, December 13th, 2018 | The Cash Flow Group | Comments Off on Knowing when You Need a South Florida Collection Agency.

As a business that deals strictly with other businesses, you would naturally expect that you would not have any problems getting your customers to pay their bills. After as your customers are other businesses, surely they understand how important it is that they pay their bills in the same way as they expect their customers do. Sadly, this is not always the case as you will find that from time to time you are going to have to hire a collection agency to recover your money.

In as much as you would like to be able to count on all of your business customers to pay all of their bills on time, there are going to be times when this just is not going to happen. When the time comes that one of your customers does not pay, you may be left with no recourse other than to contact a collection Agency such as The Cash Flow Group. We specialize in business debt collections and our team of experts will work with you and your customer to ensure that you get the money you are owed.

Thursday, December 13th, 2018 | Florida commercial collection agency | Comments Off on Is a debt as “uncollectible.” South Florida Debt Collections

South Florida Debt Collections

One question that business owners often have to wrestle with at tax time is whether or not to write off a debt as “uncollectible.”

If your business uses a cash basis accounting system, this isn’t an issue for you. In a cash basis accounting system, you don’t count money that you’re owed until it’s paid to you. You can still write off any expenses related to an unpaid invoice, but you do not owe taxes on any unpaid income. If you are a very large company this also is unlikely to be an issue for you. Large companies tend to use a reserve form of accounting and have a “bad debt reserve” to which they apply bad debts.

However, if you are neither a very large or very small company, you most likely file your taxes on an accrual basis. In accrual basis accounting, the unpaid invoice shows up as income on which you owe taxes. However, if you never collect that money, you can write off the amount as a bad debt expense.

From a tax-planning standpoint, it is usually best to take your write off as soon as possible so that you get the tax deduction now, instead of later. The only time taking the deduction later would be better is if you are expecting to be in a higher tax bracket later on. This is primarily a concern for sole proprietors and S corporations, whose annual income fluctuates more widely. However, even if you expect to change tax brackets, you can not randomly decide when to write off debts. There are no hard and fast tax rules about when you can consider a debt “uncollectible,” but the IRS does like to see consistency in your tax filing methods.

Generally, it’s hard to justify classifying a debt as “uncollectible” if the debt has been owed for less than 90 days. But, some warning signs that a debt may be uncollectible, even if it’s been less than 90 days, include a company declaring bankruptcy, a company refusing to answer communication, a company stating that they will not pay you, or a company simply disappearing. Once you have turned a debt over to a collection agency, you are also justified in writing it off on your taxes. However, if the collection agency is able to collect, you will owe taxes on the amount collected.

As a commercial collection agency, we (the cash Flow Group) recommend that you not wait until tax season to think about how you will collect on unpaid invoices. We advise clients to consider professional help with unpaid invoices that are 90 days or more overdue, or when they start to notice any of the warning signs that a business may not be willing or able to pay its bills.

Writing off bad debt is helpful to your bottom line, but what’s more helpful is actually collecting on that debt. For example, imagine that your company is in the 33% tax bracket and a company owes you $10,000. If you write that off as bad debt, you’ll save $3,300 in taxes. However, if you hire a reputable collection agency that charges 20% of the amount collected, you could get $8,000. Earning $8,000 is clearly better than saving $3,300.

Sometimes, a company that cannot pay its bills may offer you stock, or equity instead of paying what is owed. If you have a personal relationship with the company, or truly believe that their financial problems are temporary, this can be a tempting option. It may seem that by accepting stock options, equity, or other collateral, you are avoiding the hassle of collecting on the debt. Perhaps you want to give the company a chance to fix things in the hopes that may be able to make more money in the long run.

Accepting stock or equity may also feel good emotionally. No one wants to think that they’ve been misled, or that they’ve made a bad decision about when to extend credit. Unfortunately, it is rarely a good idea. For starters, unless the company is public, it is very difficult to turn your stock into cash. If the company is public and having financial difficulties, their stock is probably not worth very much.

If you are determined to pursue this idea with a company that owes you money make sure to do your due diligence. Remember, once you accept stock in place of payment, you are no longer a vendor, you’re an investor. If this company’s business model and current situation means you wouldn’t invest in them under normal circumstances, don’t do it now when they’re already in trouble. Make sure that you also research any potential tax implications, IPO plans, and the effect that not receiving money immediately will have on your own cash flow. Make sure any agreement you sign is fully reviewed by a lawyer and does not leave you responsible for other debts the company may have incurred or may incur in the future.

Most importantly, before accepting stock options or equity, make sure to consult with a commercial collection agency like The Cash Flow Group. With our years of experience, there may be things we can do to get you the money you are owed. If you want to invest in a company, make sure that you’re doing so because you believe in the company and think it’s a good investment, not because you’re desperate to resolve a difficult situation.

Tips from THE CASH FLOW GROUP a South Florida collection agency, When it comes to companies that owe you money there are two basic types, those who won’t pay and those who can’t pay. With a company that can pay, but won’t, either because they are unhappy with the work or simply want to get away without paying, it’s best to act quickly. If a company is attempting to cheat or defraud you, your best course of action is to send them to a South Florida collection agency, as quickly as possible. However, if a company wants to pay you but is having a cash flow or other financial problem, you may want to consider making a deal.

The first step in deciding whether or not to consider a deal is to get a thorough understanding of the nature of the company’s financial problems. Ideally, you would start to notice signs of financial problems with a company before the invoice was due. That way you could be prepared and even discuss the problem before the payment is late. But, if an invoice is going unpaid, especially from a formerly trusted client, you may want to get on the phone and find out what’s going on. It’s likely that your contact in Accounts Payable, or on your project, will not be willing, or able, to share the full scope of the issue. In this case, you’ll want to speak with an executive or owner, someone qualified and able to share details.

The most compelling reason to make a deal is if a deal is the only way you’ll receive any of the money that you’re owed. If a company is on the verge of bankruptcy or closure, a deal may be your only choice for getting paid. If, however, the company is experiencing a temporary cash flow problem or is likely to rebound, you may want to negotiate a new payment date and add fees or interest. Be careful though, plans to recover from a financial problem are never a sure thing. By agreeing to wait to be paid you could wind up losing the short window of time in which you could be paid. Once a company goes to bankruptcy you are unlikely to ever recoup your money.

Deciding when, how, or whether to make a deal for owed money is complicated. Most people simply do not have the legal or professional expertise to know when it is and isn’t a good idea. That’s why we always recommend consulting with a professional commercial South Florida collection agency. A reputable commercial South Florida collection agency is trained to get you more of the money you are owed than you can on your own and can save you time and irritation. If you have an account that you’re considering making a deal on, give The Cash Flow Group a call first.

Saturday, December 1st, 2018 | Florida Debt Collection | Comments Off on Collection Fees and Interest in Commercial Collections

Collection Fees and Interest in Commercial Collections

The Cash Flow Group’s goal is to try to recover your money without going to court. Yet, sometimes litigation is necessary. Clients often wonder if they can add our collection fees to the collected amount. These costs can add in specific situations.

Collection Fees and Costs

A contract between the parties that states collection fees are due in the event of late payment. After this, collection fees apply. Keep in mind that having this provision on your invoices may not be enough. Many states need you to have a document signed by your customer. This document needs to be indicating they agree to this specific provision. The Credit Application is the generally the best document in which to place this term.

Attorney Fees

Attorney fees apply if there is an attorney fee provision in a contract. There are some cases where the attorney fees are not in the contract. The judge has some discretion on whether to add those fees or not.

In many jurisdictions, the are basing the attorney fee award on a schedule. The award is not based on the contingency rate. First, you need to collect 100% of principal, interest and court costs. That is even if attorney fees are being awarded and added to the judgement. A percentage of litigation cases result in a voluntary payment for reduced a mounts. Because of this, it is rare to collect 100% of the original judgment amount. The amount includes interest and court costs in settled cases.

Thus, we often do not collect attorney fees even if they are being awarded.

Some contingency attorneys we work with structure their quotes. In these quotes, they get to keep 100% of any attorney fees. These fees are being awarded and collected. This is after all principal, interest and court costs are now recovered. Their logic is this extra incentive to collect the attorney fee award. They keep the award in full. It gives them incentive to get the interest and court costs on top of principal. This way they can then pursue this ‘bonus’ for themselves. Clients have control over two things. Whether to accept voluntary settlements or to pursue court ordered judgment collection efforts. But, this extra incentive for attorneys can help our clients.

These are a lot of factors to consider. As a result, keep this in mind when using a contingency attorney. Never expect any recovery of attorney fees when considering whether to sue or not.

Judgment Interest and Court Costs

Collection costs are not generally included in a judgment. But, a judge will generally include several things. These are pre-judgment interest, post – judgment interest, and initial court costs.

When is pre-judgement calculated? It is calculating from the original due date to the date the judgment is being issued. Either the interest rate stated on invoices or in a contract. If there is no mention of interest on the invoices or in the contract, then a judge may use the statutory rate. The statutory rate is different for each state, but is often between 6% and 10%. The judge may determine that the creditor is not entitled to pre-judgment interest. This is if there was no mention of interest in the agreement between the parties.

Post-judgment interest generally depends on the same criteria. It also accrues from the date of the judgment until paid. Sometimes the interest rate on invoices or in contracts are high or above the usury limit. The judge may now allow it or may limit interest to a lower rate.

Pre-Litigation: Collecting Interest and Collection Fees You may wonder why we rarely collect interest or collection fees even when they are in the contract. The bottom line is that if a debtor offers to pay the principal balance in full on a voluntary basis, but only if our client waives interest and collection fees, we have never had a client reject this offer and instead litigate. Litigation has up-front costs, can take months to years, has a higher contingency rate, and an uncertain outcome. The right business decision is to take the voluntary payment of principal only, instead of pursuing more amounts through the courts.

Collection Agencies

Other collection agencies may tell you that they get interest and collection fees on a regular basis. If they are collecting credit card debt, where these fees are the creditor’s business model and the consumer knows that up front, the debtor expects to pay interest and will. But on standard B2B claims, all collection agencies run into the same issue of a business negotiating to not to have to pay fees.

It’s frustrating to have spent months trying to collect money and to know that you are entitled to interest and fees that you may not be able to collect.

Saturday, December 1st, 2018 | Florida Debt Collection | Comments Off on What Your Clients Need to Know About Debt Collection

What Your Clients Need to Know About Debt Collection

One of the best ways to solve debt collection problems is to prevent them from happening in the first place. Work with your clients to notice any warning signs.

So, how can you keep up to date on every industry when you have time to run your own business? Obvious sources like reading The Wall Street Journal or listening to NPR can give you a general overview of most industries. Many larger companies use “knowledge managers” or librarians to create digest versions of relevant news. You can do something similar for yourself with daily news digests, including industry specific ones, and Google Alerts for relevant industries. Apps such as Owler, Nuzzle, and can also help you create personalized news feeds that give you the big picture you need.

If you do notice news that might have a negative impact on your client or customer, it doesn’t mean you have to cut them off or change payment terms, but depending on the news, you may wish to check in with the client or consider diversifying your client base.

Being informed about what’s going on in a variety of industries can help form better relationships with your clients. As a bonus it may also make you a more interesting guest at parties!

At The Cash Flow Group, we hope all your clients stay healthy and pay their bills on time, but if not, let us know how we can help.