Saturday, January 12th, 2019 | The Cash Flow Group | Comments Off on How To Ask Questions.?!

Here’s the premise:

Good questions directly lead to greater success in life and career;

Most people ask bad questions (myself included).

We are constantly solving problems on the job, including making the sale. We need to collect information to solve these problems. How we ask questions greatly influences the answers and our eventual success. Better questions lead to better solutions, faster, leaving more time to accomplish other goals, solve other problems, or recreate.

Time is precious and opportunities are fleeting. Walking down the hall or riding in an elevator with your boss, their boss, or your client is the perfect opportunity to learn and/or impress with a great question. A poorly worded question means a missed opportunity.

In our personal lives, well structured questions lead to better conversations and deeper emotional connection. Fortunately, learning how to better structure questions is not that difficult.

Examples Of Bad Question Techniques

Ramble;

Ask leading questions;

Ask multiple-choice questions;

Pose Yes or No questions when you need information.

When your question goes on and on, the real question gets lost and so will the answer. Rambling is often the sign of nervousness, embarrassment that you don’t know the answer, or lack of forethought about your real question and how to ask it. If you need the answer, don’t be embarrassed to ask the question.

Bad: What’s the best way for me to calculate DSO? Do you want me to use all sales? Over what period? And should I eliminate cash sales? Do I look at the last month or longer? And what about receivables that we haven’t written off by they are really old? And that large contract receivable that the sales person said we should never have booked because of the dispute that emerged only days later?

Good: How do you want me to calculate DSO?

If you ask a leading question, you are not likely to get an honest answer, and therefore you are off-track in getting to your solution. Even if you think you already know the answer or are just seeking confirmation, an objective question makes you look more confident. A leading question can make you look like a condescending jerk.

Bad: What do you think about the ugly sample logos they presented?

Good: What do you think about the sample logos?

Multiple choice questions are appropriate when you truly want the listener to choose from one of the options. But, if you are trying to learn, have a conversation, or interview someone, you lose valuable time with your extended question and tend to limit the responses.

Bad: When you saw the presentation, what captured your attention the most? The graphics and video? The speaker’s great delivery and humor? The emotional customer testimonials?

Good: When you saw the presentation, what captured your attention?

When you want to learn, you don’t want to ask a closed ended question that can be answered with a simple “yes” or “no.” Instead, you want to ask an open ended question so the person can share their thoughts and you get information.

Bad: Did you like the movie?

Good: What did you think of that movie?

Top 2 Question Tips

Stop talking at the question mark;

H5W: How, who, what, when, where, why. Start with one of these words.

Stopping your question when you get to the question mark is the opposite of rambling or asking a multiple choice question. Too often we are trying to show our knowledge or cover up our lack of knowledge with extended questions. By simply focusing on this one technique of stopping at the question mark, you will start asking better questions.

Bad: Do you have any vacation plans this summer? I know you often go to the mountains, and you have been talking a long time about going to Europe. But, you said you haven’t seen your parents in a long time, so are you going to visit them? And, didn’t you say something about one of your kids maybe having to go to summer school, so will that interfere with plans?

Good: What are your summer vacation plans?

How, who, what, when,where and why has been the staple of reporting since the infancy of journalism. It also turns out to be a better way to ask questions. Start your question with one of these 6 words, and you are more likely to get thoughtful or more revealing answers. Alternatively, journalist Shane Snow says sentences “that begin with is, are, would, should or do you think can limit your answers”. All too often these words result in leading or closed ended questions and an answer of less value.

Bad: Should the government add more laws restricting gun sales?

Good: What do you think of the current laws on gun sales?

When I’m preparing for a meeting or conversation where I know I’ll be asking a lot of questions, I’ll write on a sticky note or in my notebook:

? Stop H5W

I look at this frequently to remind myself to keep my questions in check and start with the right word.

How To Use Questions

Get Conversations Back On Track

Questions can be used for more than just learning and solving problems. Think about the interviews you’ve heard. The guest may start rambling or drift off-topic. You start to lose interest. A skilled interviewer can interject with a good question to get a conversation back on topic without seeming pushy or condescending. You can use this same technique in meetings, phone calls or personal conversations.

Sell Ideas

We all know that a great way to get buy-in to something is for the person to think it is their idea. A series of questions can get someone to see things from your perspective or arrive at the solution you desire. You don’t need to ask leading questions, just well designed objective questions. You will get better ideas and less resistance. Follow up with comments and more objective questions until their answers point to your desired result. Suddenly, it’s their idea. While this approach seems to take longer and require more effort, questions help you avoid defensiveness and resistance and often this is the fastest way to your desired result.

Resolving Disputes

I’ve been negotiating transactions and resolving disputes for over 30 years. Asking questions is one of my favorite and most successful techniques. I know that initially I have limited knowledge of the situation, and that is usually heavily weighted towards my client’s perspective. But, I can’t get a deal done or a dispute resolved until I can get both sides to the same place. Questions help me learn and people like to be heard, which is a critical step in resolving problems. If the initial answers and facts support my client’s position, I find asking additional questions is a very effective way to get the other party to an acceptable resolution.

At our collection agency, I frequently deal with clients whose customers don’t want to pay for the full amount of a long term contract. The most common reasons are: they don’t need the services any longer, they weren’t getting the sales results desired from advertising or marketing services, they didn’t cancel before it auto-renewed, or they’ve run into financial problems. The most common excuse is that our client failed to perform. Once I learn their position and underlying rationale, I’ll ask questions:

Where in the contract does it say you can cancel?

Where in the contract does our client guaranty market results?

When did you first realize there might be a performance issue?

Where is your written documentation and notice of performance failure?

What does the auto-renewal language say?

Where is your written cancellation notice?

I find that by asking questions instead of making assertions, there is less resistance, more focus on the specific point, and a realization that their legal position is precarious. They may not admit any weakness, but as long as they understand, progress has been made and the specific issue no longer needs to be addressed. Now we can focus on negotiations and a resolution.

Questions As A Negotiating Tactic

You can’t resolve a dispute if you are stuck on positions.

A few years ago a small businessman called me after his $300,000 project with a public company blew up at the last moment. Days before the project was to be completed, the legal department at the public company noticed some paperwork issues they wanted to rectify. They passed along their requests to their project manager who communicated with the vendor. While the requests seemed very reasonable to the legal department, there were a variety of reasons why they were not reasonable to the vendor. The vendor said “no” to the project manager, the legal department said “no deal” to the project manager, and a minor disaster resulted.

I got involved when the customer was demanding the return of their deposit and the vendor wanted full payment of the remaining contract balance since he had essentially fully performed. After weeks of collecting information and phone calls with the customer, I finally pieced together what happened. Regardless of the specific issues between the companies, a stalemate had ensued and the project failed because during the dispute, each side had developed a position and simply kept repeating it.

The breakthrough in my attempt to resolve the dispute came when I asked the following question to the general counsel of the public company: ‘Why didn’t someone from your department talk directly with the vendor to understand his concerns and explore alternatives?’ The attorney realized the mistake and became more open to take a different approach in the current discussions. It took some tough negotiating from there, but we eventually found a way to avoid the courtroom and my client was satisfied with the final monetary compensation.

Questions Turn Focus From Position To Underlying Objective

As in the stalemate example above, I see this Position Problem in negotiations all the time. The parties focus on positions and not on what they want to accomplish. Whether it’s an acquisition, investment, intellectual property license, or debt collection, when you get stuck on positions, you are not likely to complete a deal. All too often, each side assumes it is a zero-sum game and that moving from their current position is a loss for them and a win for the other side. That usually isn’t the case, as getting a deal done is how each side actually gets a win, and the worst thing that can happen is each side remains stuck.

Knowledge is Power

This cliche is especially true in negotiations and dispute resolution. Both sides know it and may intentionally attempt to limit the knowledge you gain or mislead to get an advantage. You typically only get a limited amount of time and number of questions to ask. The amount of knowledge you gain will be directly tied to how well you ask questions.

Preparation is an extremely valuable part of the process. I try to learn as much as I can before a negotiation session or debt collection call. This way I can focus my questions on the areas where I have limited insight or knowledge and fill in the gaps so I can devise a strategy to achieve success.

Early in my career, I would ask leading or multiple choice questions because I thought I already had certain knowledge from my research and preparation. I wanted to race to the finish line from that starting point. All too often, despite my poorly worded questions, I would learn that my assumptions were wrong and there were other reasons that lead to the dispute. Or, worse, people would go down the path of my leading question and it would be much later before I learned of the other underlying issues and concerns. So, while preparation is key, I now focus on asking questions in a better way so I get more valuable answers.

Saturday, January 12th, 2019 | The Cash Flow Group | Comments Off on “That Employee Did Not Have The Authority To Sign That Contract” and how to handle hearing it.

“That Employee Did Not Have The Authority To Sign That Contract” At he Cash flow Group we hear it all the time: “We are not going to pay those invoices because the person who signed the contract didn’t have authority.” Many go on to say: “It says right in our By-laws that only an officer can bind the company.”

This tells us several things:

The debtor does not want to pay;

The debtor is aware of this outstanding payable;

There is a good chance the debtor has the money to pay;

The debtor either does not know the law or is pretending to not know the law.

As a south Florid collection agency specializing in large claims, we know the law is on our side. But, our initial response to “That Employee Did Not Have The Authority To Sign That Contract” is not about the law, but to ask questions to learn more. We want to know why they don’t want to pay, because that is the real problem to solve.

We encounter this situation most frequently with service contracts. Typically the debtor signed up for a service of some type, such as advertising, email list access, or an information database. The most frequently explanations we hear as to why they don’t want to pay are:

We never used the service;

We didn’t get any benefit from the service;

The service didn’t work the way we thought it would;

Our business changed directions and we didn’t need the service;

Our revenue declined and we just can’t afford it.

Once we hear the explanation of why “That Employee Did Not Have The Authority To Sign That Contract”, we’ll ask a few more probing questions to fully understand the real issue we need to resolve. We also make sure to contact the client regarding the debtor’s actual usage of the service in case that information will help us with the debt collection effort.

Then we pivot to the issue of Apparent Authority, the excuse the debtor is trying to hide behind. Under the law of agency, an Agent (employee) is able to bind the Principal (company) in a contractual relationship with a third party (customer or vendor). Business could not function efficiently if purchasing people could not order supplies and if sales people could not quote prices and complete sales. While these employees may not be Agents of the company able to execute a contract to sell the entire company to someone, they typically do have the authority to bind the company to these daily transactions.

Under Apparent Authority, if it appears that the employee has authority then their actions bind the company. This appearance can be accomplished by providing the employee with company identifiable forms or stationery, a truck with a company logo, or just having them work from the company office. In all of these cases, it is reasonable for the other person to assume that this employee has authority to enter into the transaction being discussed and therefore the threshold of Apparent Authority has been met. Our client’s contract with the debtor is legally binding.

Our collection strategy will be different if we are dealing with a sophisticated business person who is just trying to show us with a bad excuse versus an unsophisticated business person who is just hoping this excuse will work. So, we typically don’t just explain the concept of Apparent Authority, but ask a series of questions to learn more about who we are dealing with while leading the debtor to this conclusion.

For example of “That Employee Did Not Have The Authority To Sign That Contract”: how many people work for the company, who purchases the office supplies, who makes the sales, where do they work from, do they have business cards or access to company stationery, do they bind the company to these transactions? From there it is easy to explain Apparent Authority and volunteer to send them links on the Internet where they can see for themselves that this is a binding contract. From that point forward, we refuse to discuss that issue and get back to the real issue of collecting the money that is legally owed.

Saturday, January 5th, 2019 | The Cash Flow Group | Comments Off on calling your customer about a past due invoice

You have been calling your customer about a past due invoice for the last month. After a couple excuses and a couple broken promises, now no one answers the phone or returns messages when you call repeatedly. What does this mean? Have they closed? Has office staff been reduced to the point there is no one to answer calls, including from potential customers?

In our experience, it is not uncommon for us to learn that they are simply not answering calls from people who might be trying to collect money. So, any ID blocked calls, and calls from known creditors are always ignored, sent to voicemail, and never returned. This is especially true when calling your customer about a past due invoice on that person’s cell phone. We know this because we frequently get through to these people by using a phone number that the debtor will not recognize and they answer.

When implementing this strategy, we usually first call with our regular unblocked phone number and get the typical ignoring treatment. Then 10 minutes later we call with an unblocked but unidentified number. That way we know that the only reason they answered is they didn’t know it was not us who was calling.

As a collection agency, if someone answers an alternative phone, we know that this may be the last time we get to talk to the person. We very quickly deliver a firm message that we have now proven they have been ignoring us, and that if they do that anymore, we have no choice but to send their file to the attorney. For an in house debt collector, the message should be that their file will be sent to a collection agency and reported to credit bureaus and groups if that has not yet happened. We find that people are more likely to answer if the unidentified phone has an area code from the same region as the debtor. But, we find even cross country area codes can work, now that people keep cell phone numbers as they move about the country.

There are many ways to get low cost access to an unidentified phone for calling your customer about a past due invoice number. For under $20 initial cost, and as little as $10 a month, you can have a prepaid cell phone with any area code in the country. That’s a small investment to be able to get through to one or more customers who owe you money and are ignoring all your calls.

Once you get through, if you don’t get cooperation, you know you will never get paid unless you take other action. Just having that knowledge earlier is well worth the minor cost of getting an alternative number. We all know that the chances of collecting decline dramatically the longer an invoice is not paid.

So, the sooner you know they are ignoring you, and the sooner you take more aggressive action, the more likely you can still get a recovery.

Saturday, January 5th, 2019 | The Cash Flow Group | Comments Off on End of Year Tasks for your Business

The end of the year always brings some predictable events. You know that magazines and websites will be releasing their lists of “best movies” or “most memorable events.” You know that car dealers and other large item retailers will be trying to sell off expensive merchandise. You know payroll departments will be preparing to fill out W-2 forms, and accountants will be getting ready for tax season. As a commercial collection agency there are certain tasks we’d love to see business owners add to their annual end of the year to-do lists.

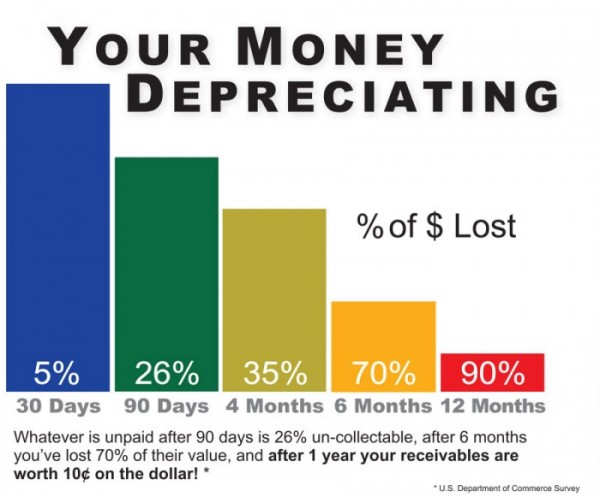

Determine Which Invoices Need Attention Once an account is 90 days overdue, there’s already a 26% chance that it will never get paid. At 7 months overdue, there’s only a 50% chance that you will get paid. Ideally, business owners would routinely check for late invoices and turn them over to a reputable collection agency while there was still a great chance of getting the invoice paid. But at the very least, reviewing past due invoices is something that should be end of year tasks for your business.

Update Terms and Conditions The world has changed a lot in the last five years. If you haven’t updated your terms and conditions on credit applications recently it may be time to make a change. Our free handbooks on Credit Applications and Terms and Conditions may not be the books you want to cozy up with by the fire, but they may save you money in the year ahead.

Review Procedures Are your internal collection policies and procedures working? Can you make changes to improve efficiency and effectiveness? Are you making phone calls when you should be writing emails to get answers in writing? Are you writing emails when you should be making phone calls? Is there anything you could automate, such as overdue notices, which would make life easier for your Accounts Receivable department? An annual review of your policies and procedures may help you identify both problem areas and strengths.

Update Payment Procedures Strangely enough, many businesses, especially smaller ones, often make it difficult for clients to pay them. If you’ve resisted allowing online credit card transactions, or PayPal transactions because of fees, it’s time to rethink those ideas. Services such as PayPal and Square may make your business more time efficient. Don’t forget to update your check payment procedures as well. Services like Vericheck can help you avoid accepting bad payments.

Check on Your Providers When you hire a lawyer or a credit collection agency you’re hiring a company that will represent you. The last thing you need is someone from outside your company creating legal or reputation hassles for you. Your end of year tasks for your business is a great time to check in with the reputation of any service provider that represents you. Check Better Business Bureau ratings, online reviews, and professional organization memberships.

The end of the year is a busy time and adding more “to dos” to your existing task list can be daunting. But, making sure that you’re on top of unpaid invoices and payment policies can be a great way to ensure that you start the next year off right. If you’re end of the year tasks reveal debts you need help collecting, make sure to let us know, we’re here to help.

Thursday, December 13th, 2018 | The Cash Flow Group | Comments Off on Knowing when You Need a South Florida Collection Agency.

As a business that deals strictly with other businesses, you would naturally expect that you would not have any problems getting your customers to pay their bills. After as your customers are other businesses, surely they understand how important it is that they pay their bills in the same way as they expect their customers do. Sadly, this is not always the case as you will find that from time to time you are going to have to hire a collection agency to recover your money.

In as much as you would like to be able to count on all of your business customers to pay all of their bills on time, there are going to be times when this just is not going to happen. When the time comes that one of your customers does not pay, you may be left with no recourse other than to contact a collection Agency such as The Cash Flow Group. We specialize in business debt collections and our team of experts will work with you and your customer to ensure that you get the money you are owed.

Tips from THE CASH FLOW GROUP a South Florida collection agency, When it comes to companies that owe you money there are two basic types, those who won’t pay and those who can’t pay. With a company that can pay, but won’t, either because they are unhappy with the work or simply want to get away without paying, it’s best to act quickly. If a company is attempting to cheat or defraud you, your best course of action is to send them to a South Florida collection agency, as quickly as possible. However, if a company wants to pay you but is having a cash flow or other financial problem, you may want to consider making a deal.

The first step in deciding whether or not to consider a deal is to get a thorough understanding of the nature of the company’s financial problems. Ideally, you would start to notice signs of financial problems with a company before the invoice was due. That way you could be prepared and even discuss the problem before the payment is late. But, if an invoice is going unpaid, especially from a formerly trusted client, you may want to get on the phone and find out what’s going on. It’s likely that your contact in Accounts Payable, or on your project, will not be willing, or able, to share the full scope of the issue. In this case, you’ll want to speak with an executive or owner, someone qualified and able to share details.

The most compelling reason to make a deal is if a deal is the only way you’ll receive any of the money that you’re owed. If a company is on the verge of bankruptcy or closure, a deal may be your only choice for getting paid. If, however, the company is experiencing a temporary cash flow problem or is likely to rebound, you may want to negotiate a new payment date and add fees or interest. Be careful though, plans to recover from a financial problem are never a sure thing. By agreeing to wait to be paid you could wind up losing the short window of time in which you could be paid. Once a company goes to bankruptcy you are unlikely to ever recoup your money.

Deciding when, how, or whether to make a deal for owed money is complicated. Most people simply do not have the legal or professional expertise to know when it is and isn’t a good idea. That’s why we always recommend consulting with a professional commercial South Florida collection agency. A reputable commercial South Florida collection agency is trained to get you more of the money you are owed than you can on your own and can save you time and irritation. If you have an account that you’re considering making a deal on, give The Cash Flow Group a call first.

Every single business owner in the US has experienced problems with nonpaying clients. The following shoes the worrying statistics once an invoice is delinquent. Collecting on the debt decreases by more than 1 percent every week the debt remains unpaid. Once the invoice is 90 days overdue, you have less than a 70 percent chance of collection. This drops to almost half once the invoice is six months overdue. Rapid action is necessary and taking steps could improve the situation. Consider putting in place a B2B online payment processor.

The key to resolving nonpayment issues is to look for the red flags. Flags that show a client could be in trouble before a company even misses a payment. Here are some top things to look for that can show future payment problems.

Red Flag Signs

The company is changing locations. It’s expensive to move, so you need to look at the reasons behind it. Is it a smaller location? If so, that could point towards financial problems resulting in downsizing. If it’s a bigger location, that could be a good sign. Financing expansion is often at the expense of companies that the company deals with.

The company is laying off workers. The cause of this is usually financial problems. You may notice that an employee you usually deal with has disappeared. This could be a sign that he or she has moved on to a more reliable workplace before the company goes out of business.

The business is being sold. Usually, a business is only sold when financial difficulties are being experienced. When the company sells, collecting on overdue invoices becomes harder than ever.

Personal problems. If your client is running a small business, problems could take priority over overdue invoices. Problems such as marital difficulties or an illness,

Excuses. You may here, “We can’t find the invoice.” “The invoice isn’t approved yet.” “The person responsible for signing checks isn’t in the office at the moment.” This could be a subtle indicator that all isn’t right at the client’s end.

What to Do When You Spot A Red Flag?

If you recognize any of these signs from one of your customers, it’s time to get some answers. Call the client and find out more about the situation. Whenever possible, speak to several people. Then you can determine the consistency of the story. If possible, go to the client’s premises and find out the extent of the problem.

If you suspect there is a red-flag situation with one of your clients, you need to take aggressive action. If not, you won’t receive a payment quick, or, even, at all. Give the account extra attention and avoid waiting around to see what happens.

How to Improve Chances of Payment

One of the best ways to improve the chance of payment is to put in place a B2B online payment processor. This makes the process of paying for goods and services a lot simpler and more convenient. Use An online payment portal that accepts many payment methods. A portal can make the difference between receiving payments on time and having to chase nonpaying customers. Also, put in place the facility to take payments over the telephone. During collections, telephone conversations will help to improve cash flow with real-time authorizations. This way you don’t have to rely on waiting for the client to write a check.

Call the Cash Flow Group today with any questions or concerns you might have. We look forward to hearing from you!

Having a small business can be a very exciting venture. There are also many tedious procedures. You need to follow these procedures so the business can function well. Being a business owner is a major responsibility. Even if that business is small. It can be a very steep learning curve to discover how to best manage and run that business. All this sounds daunting, but there is good news! There are many service providers that can help you manage the different elements of your organization. While there is any number of things that your business will need to be a success, three are of key importance. They may not be especially exciting, but they are vital. Business owners tend to overlook them at their peril. The key elements are business insurance, accounting services, and online payment processing. These are for all small business owners. Let’s take a look at why each is important and why you should make sure you have them in place.

Accounting Services

Having good accounting services is key to your business’ success. This goes for whatever type of company you have and whatever size it is. Accounting is vital to keep track of all your company’s accounts. Equity, liabilities, and assets and for any business to function well. Having a strong grip on how, why, and where money goes. You can opt for online accounts services. Or use the services of accounts to keep this information within easy reach. Keep on top of all transactions. This way you can plan your budget, report your profits, and keep investments in your company with ease.

Business Insurance

Car insurance helps drivers if they have an accident. Business insurance is essential to protect your business in case something goes wrong. Being prepared for a worst-case scenario is essential. Having a backup plan is as essential should anything go wrong. There are many kinds of business insurance. Insurance including fire, hazard, unemployment, and workers’ comp. Making sure you have the ones that are most appropriate to you in place is essential. Insurance is all the well-being of your business.

Tips for Successful Debt Collection by Phone and Email

What is one of the biggest mistakes you can make? People try to collect an unpaid debt while communicating in an unprofessional manner. Being in debt and collecting debt can both be stressful situations. There are many laws around debt communications.

Phone Calls

The phone is generally seen as the most effective and efficient way of collecting an unpaid debt. Some general rules to follow:

Be polite and professional.

No gum chewing, eating, or web surfing while calling. Use please and thank you, and introduce yourself. One trick receptionists have used for years is to smile while on the phone.

Call at the right time of day. Some people work mornings, others don’t come into the office until the afternoon. By knowing when the debtor is available to talk on the phone, you can avoid playing phone tag. Ask the debtor what time they are generally available. Doing this can save a significant amount of time.

Take notes or record conversations.

If you are going to record a conversation, you must get permission first. But taking notes can be effective. By keeping a log of any agreements or issues, you can avoid repeating what you have already said. After the call, send an email summarizing the conversation and any commitments so there are no disagreements later.

Be careful about leaving messages.

It is very important that debt collectors never disclose private information. As a general rule when collecting from individuals, collectors should assume that any voicemail messages they leave will be heard by somebody other than the debtor. If it is a business debt, full detail can be left on any business phone number and personal phone known to belong to a involved party.

Don’t blame or shame.

Having unpaid bills is stressful. It is not helpful to blame the debtor or imply that they have failed by not upholding their commitment to pay. Doing so will only make them upset and less willing to pay. Speak and find out why the debtor hasn’t paid their bills, and then try to work towards a solution to the problem. If they have a complaint about the product or service, find out why and try to resolve the complaint. If the customer doesn’t have the money at that time, ask them to prove this and have them suggest a solution. Forcing the debtor into a payment plan they know will default on will likely cause the debtor to be less interested in working with you.

Email

Although phone conversations are the preferred method for discussing unpaid debt, email also has an important role to play, especially when documents are being requested or sent, a paper trail is needed, or for quick follow ups and reminders.

If you can’t write, don’t.

Everybody knows their own skill set. If you are not a good writer, please do not write your own emails. Instead consider hiring an in-house or freelance copywriter to create a set of email templates for you that will help you communicate.

Be polite and professional.

Because tone of voice is so hard to determine in an email it’s especially important that you be polite and professional. Do not attempt to joke or be lighthearted about the situation. Keep your messages short and ensure they only emphasize the point you want. Shorter emails are more likely to be read in their entirety, and if you make the message you want to send to the recipient very clear they’ll be sure to get the point.

Being polite also includes responding to emails on time. If you want someone to respond to your emails, you must do the same for them.

Create a factual and short subject line. Your recipient will be far more likely to open the email if they know what it’s about.

Don’t send the message to people who don’t need to see it.Remember that any email communication can be used in a lawsuit if the debtor sues you for disclosing information to parties against regulation (especially in the case of consumer collections). Email communications are permanent, and the debtor will be able to find a copy of the message stored online with ease.

Communications are one of the tricky elements that sometimes makes it easier to hire a professional collection agency. If you’re having trouble finding the right way to talk to debtors, please give us a call.

When it comes to companies that owe you money there are two basic types, those who won’t pay and those who can’t pay. With a company that can pay, but won’t, either because they are unhappy with the work or want to get away without paying, it’s best to act . If a company is attempting to cheat or defraud you, your best course of action is to send them to a collection agency, as as possible. Yet, if a company wants to pay you but is having a cash flow or other financial problem, you may want to consider making a deal.

Commercial collection agency

The first step in deciding whether to consider a deal is to get a thorough understanding of the nature of the company’s financial problems. , you would start to notice signs of financial problems with a company before the invoice was due. That way you could be ready and even discuss the problem before the payment is late. But, if an invoice is going unpaid, especially from a trusted client, you may want to get on the phone and find out what’s going on. It’s likely that your contact in Accounts Payable, or on your project, will not be willing, or able, to share the full scope of the issue. In this case, you’ll want to speak with an executive or owner, someone qualified and able to share details.

Sometimes making a deal is the only way to receive payments. If a company is on the verge of bankruptcy or closure, a deal may be your only choice for getting paid. If the company is experiencing a temporary cash flow problem, you may want to negotiate a new payment date and add fees or interest. Be careful though, plans to recover from a financial problem are never a sure thing. By agreeing to wait for payment you could lose time in which you could receive. Once a company goes to bankruptcy you are unlikely to ever recoup your money.

Deciding when, how, or whether to make a deal for owed money can be overwhelming. Most people do not have the legal or professional expertise to know when it is and isn’t a good idea. That’s why we always recommend consulting with a professional commercial collection agency. A commercial collection agency will help get the money you’re owed. If you have an account that you’re considering making a deal on, give us a call first.